Publications

My research field is a unified econometric perspective on multilevel factor structures, long-memory dynamics, stress-testing frameworks, and macro-financial transmission mechanisms.

Explore my research output by year, or browse a curated selection of highlighted publications.

Rodríguez-Caballero, C.V., & Ruiz, E.

Annals of Applied Statistics, 2026. [Forthcoming]

We propose a Multi-level Dynamic Factor Model (ML-DFM) to capture the common global and region-specific stochastic trends in monthly centre and log-range temperatures observed at 68 locations across the Iberian Peninsula from January 1930 to December 2020. The specification of common trends is based on the analysis of temperatures at each location using unobserved component models, which decompose temperatures into trend, seasonal, and transitory components. First, we show that the centre and logrange temperatures evolve independently. Second, we remove the seasonal component before analysing common trends. Third, we find that centre temperature trends are well approximated by a smooth, integrated random walk with a time-varying slope. In contrast, a stochastic level better captures the dynamics of the log-range. The ML-DFM is estimated using an EM algorithm extended here to accommodate non-stationary factors. We show that although the commonality in centre-temperature trends is considerable, the regional components remain relevant, particularly at the log-range.

@article{rodriguez2024temperature,

title={Temperature in the Iberian Peninsula: Trend, seasonality, and heterogeneity},

author={Rodr{\'\i}guez-Caballero, C Vladimir and Ruiz, Esther},

journal={arXiv preprint arXiv:2406.14145},

year={2024}

}

}

Garrón, I., Rodríguez-Caballero, C.V., & Ruiz, E.

International Journal of Forecasting, 2026. [Forthcoming]

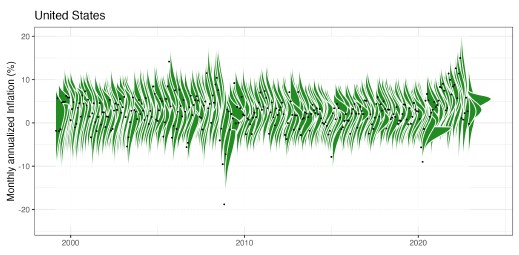

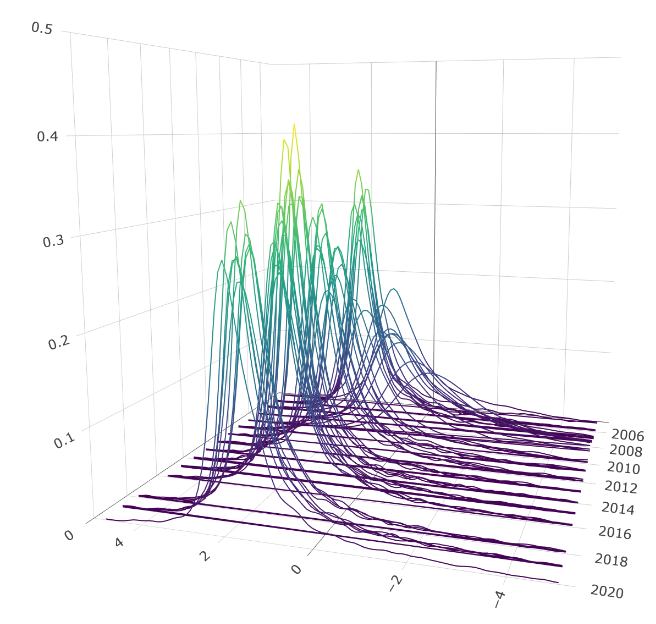

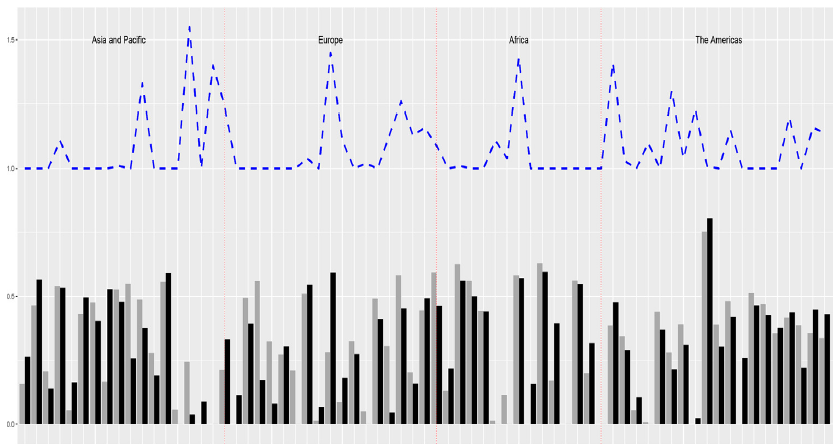

Assessing the risks of having either very low or very high inflation is crucial for policy makers, businesses, and house holders. In a globalised world, these risks are increasingly determined by international conditions. In this paper, we analyse empirically the impact of international inflation factors on forecasting monthly domestic inflation risks in a large number of economies observed worldwide from 1999 to 2022. Risk forecasts are obtained using factor-augmented quantile regressions estimated with international factors extracted from a multi-level Dynamic Factor Model with overlapping blocks of inflation corresponding to economies grouped either in a given geographical region or according to their development level. We conclude that, in a large number of countries, international factors are relevant to explain the right tail of the distribution of inflation, and, consequently, they are more relevant for the risk related to high inflation than for low inflation. The role of international factors is stronger in European developed countries, while inflation risks of developing low-income countries are hardly affected by international conditions, and the results for middle-income countries are mixed. We also show that the predictive power of international factors has increased in the most recent years of high inflation.

@article{GARRON2026,

title = {International factors and inflation risks},

journal = {International Journal of Forecasting},

year = {2026},

author = {Ignacio Garrón and Vladimir Rodríguez-Caballero and Esther Ruiz},

}

Gonzalez-Rivera, G., Rodríguez-Caballero, C.V., & Ruiz, E.

Journal of Applied Econometrics, 2024.

We propose the construction of conditional growth densities under stressed factor scenarios to assess the level of exposure of an economy to small probability but potentially catastrophic economic and/or financial scenarios, which can be either domestic or international. The choice of severe yet plausible stress scenarios is based on the joint probability distribution of the underlying factors driving growth, which are extracted with a multilevel dynamic factor model (DFM) from a wide set of domestic/worldwide and/or macroeconomic/financial variables. All together, we provide a risk management tool that allows for a complete visualization of the dynamics of the growth densities under average scenarios and extreme scenarios. We calculate growth-in-stress (GiS) measures, defined as the 5% quantile of the stressed growth densities, and show that GiS is a useful and complementary tool to growth-at-risk (GaR) when policymakers wish to carry out a multidimensional scenario analysis. The unprecedented economic shock brought by the COVID-19 pandemic provides a natural environment to assess the vulnerability of US growth with the proposed methodology.

@article{gonzalez2024expecting,

title={Expecting the unexpected: Stressed scenarios for economic growth},

author={Gonz{\'a}lez-Rivera, Gloria and Rodr{\'\i}guez-Caballero, C Vladimir and Ruiz, Esther},

journal={Journal of Applied Econometrics},

volume={39},

number={5},

pages={926--942},

year={2024},

publisher={Wiley Online Library}}

Ergemen, Yunus Emre & Rodríguez-Caballero, C.V..

International Journal of Forecasting, 2023.

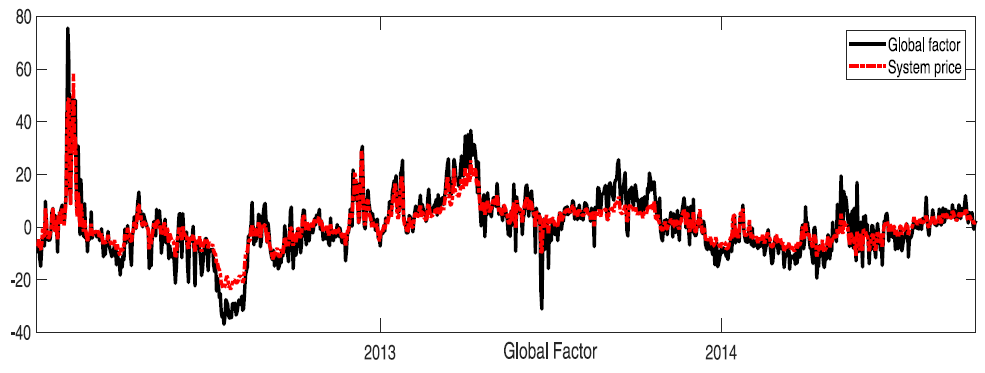

A dynamic multi-level factor model with possible stochastic time trends is proposed. In the model, long-range dependence and short memory dynamics are allowed in global and local common factors as well as model innovations. Estimation of global and local common factors is performed on the prewhitened series, for which the prewhitening parameter is estimated semiparametrically from the cross-sectional and local average of the observable series. Employing canonical correlation analysis and a sequential least-squares algorithm on the prewhitened series, the resulting multi-level factor estimates have centered asymptotic normal distributions under certain rate conditions depending on the bandwidth and cross-section size. Asymptotic results for common components are also established. The selection of the number of global and local factors is discussed. The methodology is shown to lead to good small-sample performance via Monte Carlo simulations. The method is then applied to the Nord Pool electricity market for the analysis of price comovements among different regions within the power grid. The global factor is identified to be the system price, and fractional cointegration relationships are found between local prices and the system price, motivating a long-run equilibrium relationship. Two forecasting exercises are then discussed.

@article{ergemen2023estimation,

title={Estimation of a dynamic multi-level factor model with possible long-range dependence},

author={Ergemen, Yunus Emre and Rodr{\'\i}guez-Caballero, C Vladimir},

journal={International Journal of Forecasting},

volume={39},

number={1},

pages={405--430},

year={2023},

publisher={Elsevier}

}

Rodríguez-Caballero, C.V..

Econometrics and Statistics, 2021.

A fractionally integrated panel data model with a multi-level cross-sectional dependence is proposed. Such dependence is driven by a factor structure that captures comovements between blocks of variables through top-level factors, and within these blocks by non-pervasive factors. The model can include stationary and non-stationary variables, which makes it flexible enough to analyze relevant dynamics that are frequently found in macroeconomic and financial panels. The estimation methodology is based on fractionally differenced block-by-block cross-sectional averages. Monte Carlo simulations suggest that the procedure performs well in typical samples sizes. This methodology is applied to study the long-run relationship between energy consumption and economic growth. The main results suggest that estimates in some empirical studies may have some positive biases caused by neglecting the presence non-pervasive cross-sectional dependence and long-range dependence processes.

@article{rodriguez2022energy,

title={Energy consumption and GDP: a panel data analysis with multi-level cross-sectional dependence},

author={Rodr{\'\i}guez-Caballero, Carlos Vladimir},

journal={Econometrics and Statistics},

volume={23},

pages={128--146},

year={2022},

publisher={Elsevier}

}

Rodríguez-Caballero, C.V. & Caporin, M.

Journal of International Financial Markets, Institutions and Money, 2019.

We introduce a novel multilevel factor model that allows for the presence of global and pervasive factors, local factors and semi-pervasive factors, and that captures common features across subsets of the variables of interest. We develop a model estimation procedure and provide a simulation experiment addressing the consistency of our proposal. We complete the analyses by showing how our multilevel model might explain on the commonality across CDS premiums at the global level. In this respect, we cluster countries by either the Debt/GDP ratio or by sovereign ratings. We show that multilevel models are easier to interpret compared with factor models based on principal component analysis. Finally, we experiment how the multilevel model might allow the recovery of the risk contribution due to the latent factors within a basket of country CDS.

@article{rodriguez2019multilevel,

title={A multilevel factor approach for the analysis of CDS commonality and risk contribution},

author={Rodr{\'\i}guez-Caballero, Carlos Vladimir and Caporin, Massimiliano},

journal={Journal of International Financial Markets, Institutions and Money},

volume={63},

pages={101144},

year={2019},

publisher={Elsevier}

}

Rodríguez-Caballero, C.V., & Ruiz, E.

Annals of Applied Statistics, 2026. [Forthcoming]

We propose a Multi-level Dynamic Factor Model (ML-DFM) to capture the common global and region-specific stochastic trends in monthly centre and log-range temperatures observed at 68 locations across the Iberian Peninsula from January 1930 to December 2020. The specification of common trends is based on the analysis of temperatures at each location using unobserved component models, which decompose temperatures into trend, seasonal, and transitory components. First, we show that the centre and logrange temperatures evolve independently. Second, we remove the seasonal component before analysing common trends. Third, we find that centre temperature trends are well approximated by a smooth, integrated random walk with a time-varying slope. In contrast, a stochastic level better captures the dynamics of the log-range. The ML-DFM is estimated using an EM algorithm extended here to accommodate non-stationary factors. We show that although the commonality in centre-temperature trends is considerable, the regional components remain relevant, particularly at the log-range.

@article{rodriguez2024temperature,

title={Temperature in the Iberian Peninsula: Trend, seasonality, and heterogeneity},

author={Rodr{\'\i}guez-Caballero, C Vladimir and Ruiz, Esther},

journal={arXiv preprint arXiv:2406.14145},

year={2024}

}

}

Garrón, I., Rodríguez-Caballero, C.V., & Ruiz, E.

International Journal of Forecasting, 2026. [Forthcoming]

Assessing the risks of having either very low or very high inflation is crucial for policy makers, businesses, and house holders. In a globalised world, these risks are increasingly determined by international conditions. In this paper, we analyse empirically the impact of international inflation factors on forecasting monthly domestic inflation risks in a large number of economies observed worldwide from 1999 to 2022. Risk forecasts are obtained using factor-augmented quantile regressions estimated with international factors extracted from a multi-level Dynamic Factor Model with overlapping blocks of inflation corresponding to economies grouped either in a given geographical region or according to their development level. We conclude that, in a large number of countries, international factors are relevant to explain the right tail of the distribution of inflation, and, consequently, they are more relevant for the risk related to high inflation than for low inflation. The role of international factors is stronger in European developed countries, while inflation risks of developing low-income countries are hardly affected by international conditions, and the results for middle-income countries are mixed. We also show that the predictive power of international factors has increased in the most recent years of high inflation.

@article{GARRON2026,

title = {International factors and inflation risks},

journal = {International Journal of Forecasting},

year = {2026},

author = {Ignacio Garrón and Vladimir Rodríguez-Caballero and Esther Ruiz},

}

de Juan, A., Poncela, P., Rodríguez-Caballero, C.V., & Ruiz, E.

International Review of Environmental and Resource Economics, 2025.

The links between climate change and economic activity have a critical relevance for the well-being of future generations. Consequently, many publications are devoted to understanding and measuring them. This paper is a comprehensive survey of recent contributions using econometric methods. We update previous surveys focusing on partial aspects of the complex relationships linking the economy and climate change. Starting from economic activity, the channels that relate it to climate change are energy consumption and the consequent pollution. Hence, we first describe the main econometric contributions of the interactions between economic activity and energy consumption, then explain the contributions and interactions of economic activity to pollution. Finally, we look at the main results on the relationship between climate change and economic activity. A necessary consequence of climate change is the increasing occurrence of extreme weather phenomena. Therefore, we also survey contributions on the economic effects of catastrophic climate phenomena.

@article{IRERE-176,

url = {http://dx.doi.org/10.1561/101.00000176},

year = {2025},

volume = {19},

journal = {International Review of Environmental and Resource Economics},

title = {Economic Activity and Climate Change},

doi = {10.1561/101.00000176},

issn = {1932-1465},

number = {2},

pages = {159-226},

author = {Aránzazu de Juan and Pilar Poncela and C. Vladimir Rodríguez-Caballero and Esther Ruiz}}

Gonzalez-Rivera, G., Rodríguez-Caballero, C.V., & Ruiz, E.

Journal of Applied Econometrics, 2024.

We propose the construction of conditional growth densities under stressed factor scenarios to assess the level of exposure of an economy to small probability but potentially catastrophic economic and/or financial scenarios, which can be either domestic or international. The choice of severe yet plausible stress scenarios is based on the joint probability distribution of the underlying factors driving growth, which are extracted with a multilevel dynamic factor model (DFM) from a wide set of domestic/worldwide and/or macroeconomic/financial variables. All together, we provide a risk management tool that allows for a complete visualization of the dynamics of the growth densities under average scenarios and extreme scenarios. We calculate growth-in-stress (GiS) measures, defined as the 5% quantile of the stressed growth densities, and show that GiS is a useful and complementary tool to growth-at-risk (GaR) when policymakers wish to carry out a multidimensional scenario analysis. The unprecedented economic shock brought by the COVID-19 pandemic provides a natural environment to assess the vulnerability of US growth with the proposed methodology.

@article{gonzalez2024expecting,

title={Expecting the unexpected: Stressed scenarios for economic growth},

author={Gonz{\'a}lez-Rivera, Gloria and Rodr{\'\i}guez-Caballero, C Vladimir and Ruiz, Esther},

journal={Journal of Applied Econometrics},

volume={39},

number={5},

pages={926--942},

year={2024},

publisher={Wiley Online Library}}

Caporin, M., Rodríguez-Caballero, C.V., & Ruiz, E.

Empirical Economics, 2024.

In this paper, we consider a fractionally integrated multi-level dynamic factor model (FI-ML-DFM) to represent commonalities in the hourly evolution of realized volatilities of several international exchange rates. The FI-ML-DFM assumes common global factors active during the 24 h of the day, accompanied by intermittent factors, which are active at mutually exclusive times. We propose determining the number of global factors using a distance among the intermittent loadings. We show that although the bulk of common dynamics of exchange rates realized volatilities can be attributed to global factors, there are non-negligible effects of intermittent factors. The effect of the COVID-19 on the realized volatility comovements is stronger on the first global-in-time factor, which shows a permanent increase in the level. The effects on the second global factor and on the intermittent factors active when the EU, UK and US markets are operating are transitory lasting for approximately a year after the pandemic starts. Finally, there seems to be no effect of the pandemic neither on the third global factor nor on the intermittent factor active when the markets in Asia are operating.

@article{caporin2024factor,

title={The factor structure of exchange rates volatility: global and intermittent factors},

author={Caporin, Massimiliano and Rodr{\'\i}guez-Caballero, C Vladimir and Ruiz, Esther},

journal={Empirical Economics},

volume={67},

number={1},

pages={31--45},

year={2024},

publisher={Springer}}

Ergemen, Yunus Emre & Rodríguez-Caballero, C.V..

International Journal of Forecasting, 2023.

A dynamic multi-level factor model with possible stochastic time trends is proposed. In the model, long-range dependence and short memory dynamics are allowed in global and local common factors as well as model innovations. Estimation of global and local common factors is performed on the prewhitened series, for which the prewhitening parameter is estimated semiparametrically from the cross-sectional and local average of the observable series. Employing canonical correlation analysis and a sequential least-squares algorithm on the prewhitened series, the resulting multi-level factor estimates have centered asymptotic normal distributions under certain rate conditions depending on the bandwidth and cross-section size. Asymptotic results for common components are also established. The selection of the number of global and local factors is discussed. The methodology is shown to lead to good small-sample performance via Monte Carlo simulations. The method is then applied to the Nord Pool electricity market for the analysis of price comovements among different regions within the power grid. The global factor is identified to be the system price, and fractional cointegration relationships are found between local prices and the system price, motivating a long-run equilibrium relationship. Two forecasting exercises are then discussed.

@article{ergemen2023estimation,

title={Estimation of a dynamic multi-level factor model with possible long-range dependence},

author={Ergemen, Yunus Emre and Rodr{\'\i}guez-Caballero, C Vladimir},

journal={International Journal of Forecasting},

volume={39},

number={1},

pages={405--430},

year={2023},

publisher={Elsevier}

}

López-Marmolejo, A, & Rodríguez-Caballero, C.V..

Regional Statistics, 2023.

Women's participation in the labour market in Central America, Panama, and the Dominican Republic (CAPADOM) is low by international standards. Increasing their participation is a goal of many policymakers who want to improve women's access to quality employment. This study uses data from CAPADOM to assess whether gender equality in the law increases women's participation in the labour force and, if that is the case, the extent to which this boosts GDP per capita. To do so, the authors use a panel VAR model. The results show that CAPADOM could increase female labour participation rate by 6 percentage points (pp) and GDP per capita by 1 pp by introducing gender-related legal changes such as equal pay for equal work, paid parental leave, and allowing women to do all the same jobs as men.

@article{lopez2023assessing,

title={Assessing the effect of gender-related legal reforms on female labour participation and GDP per capita in the Central American region.},

author={L{\'o}pez-Marmolejo, Arnoldo and Rodr{\'\i}guez-Caballero, C Vladimir},

journal={Regional Statistics},

volume={13},

number={3},

year={2023}}

Rodríguez-Caballero, C.V. & Villanueva-Domínguez, Mauricio

Empirical Economics, 2022.

Financial history shows that there is a deep-rooted human urge to make quick profits. Speculative bubbles are intrinsically involved in bitcoins and may precede striking crashes as that occurred on December 22, 2017. In this paper, we propose an econometric methodology to estimate the most likely crash date of the bitcoin bubble of 2017.We date the crash on December 13, 2017, just four days before reaching the maximum price. Nine days after, the bitcoin price fell 45% from its peaks.

@article{rodriguez2022predicting,

title={Predicting cryptocurrency crash dates},

author={Rodr{\'\i}guez-Caballero, C Vladimir and Villanueva-Dom{\'\i}nguez, Mauricio},

journal={Empirical Economics},

volume={63},

number={6},

pages={2855--2873},

year={2022},

publisher={Springer}

}

de la Escosura, Leandro Prados & Rodríguez-Caballero, C.V..

Explorations in Economic History, 2022.

This paper contributes to the debate on Europe’s modern economic growth using the statistical concept of long-range dependence. Different regimes, defined as periods between two successive endogenously estimated structural shocks, matched episodes of pandemics and war. The most persistent shocks occurred at the time of the Black Death and the twentieth century’s world wars. Our findings confirm that the Black Death often resulted in higher income levels but reject the view of a uniform long-term response to the Plague. In fact, we find a negative impact on incomes in non-Malthusian economies. In the North Sea Area (Britain and the Netherlands), the Plague was followed by positive trend growth in output per capita and population, heralding the onset of modern economic growth and the Great Divergence in Eurasia.

@article{de2022war,

title={War, pandemics, and modern economic growth in Europe},

author={de la Escosura, Leandro Prados and Rodr{\'\i}guez-Caballero, C Vladimir},

journal={Explorations in Economic History},

volume={86},

pages={101467},

year={2022},

publisher={Elsevier}}

Rodríguez-Caballero, C.V. & Vera-Valdés, J. Eduardo.

Econometrics, 2021.

This paper tests if air pollution serves as a carrier for SARS-CoV-2 by measuring the effect of daily exposure to air pollution on its spread by panel data models that incorporates a possible commonality between municipalities. We show that the contemporary exposure to particle matter is not the main driver behind the increasing number of cases and deaths in the Mexico City Metropolitan Area. Remarkably, we also find that the cross-dependence between municipalities in the Mexican region is highly correlated to public mobility, which plays the leading role behind the rhythm of contagion. Our findings are particularly revealing given that the Mexico City Metropolitan Area did not experience a decrease in air pollution during COVID-19 induced lockdowns.

@article{rodriguez2021air,

title={Air pollution and mobility, what carries COVID-19?},

author={Rodr{\'\i}guez-Caballero, C Vladimir and Vera-Vald{\'e}s, J Eduardo},

journal={Econometrics},

volume={9},

number={4},

pages={37},

year={2021},

publisher={MDPI}

}

López-Marmolejo, Arnoldo, Rodríguez-Caballero, C.V. & Ventosa-Santaularia, Daniel.

Economics Bulletin, 2021.

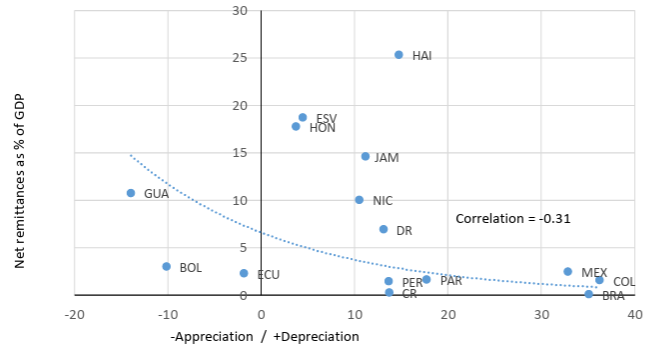

With remittances reaching historic highs in many Latin American countries, this paper evaluates the existence of Dutch disease in that region on a country-by-country basis. To do so, we employ heterogeneous panel data models with cross-sectional dependence to estimate the determinants of the real exchange rate and calculate the effect of net remittance flows in the region by country. In this context, various countries' future economic development must address this potential loss of competitiveness.

@article{lopez2021remittances,

title={Remittances at record highs in Latin America: Time to revisit the Dutch disease},

author={López-Marmolejo, Arnoldo and Rodríguez-Caballero, Carlos Vladimir and Ventosa-Santaularia, Daniel},

journal={Economics Bulletin},

volume={41},

number={3},

pages={2003--2011},

year={2021},

publisher={Economics Bulletin}

}

Rodríguez-Caballero, C.V. & Vera-Valdés, J. Eduardo.

Atmósfera, 2021.

This paper analyzes the relation between COVID-19, air pollution, and public transport mobility in the Mexico City Metropolitan Area (MCMA). We test if the restrictions to economic activity introduced to mitigate the spread of COVID-19 are associated with a structural change in air pollution levels and public transport mobility. Our results show that mobility in public transportation was significantly reduced following the government’s recommendations. Nonetheless, we show that the reduction in mobility was not accompanied by a reduction in air pollution. Furthermore, Granger-causality tests show that the precedence relation between public transport mobility and air pollution disappeared as a product of the restrictions. Thus, our results suggest that air pollution in the MCMA seems primarily driven by industry and private car usage. In this regard, the government should redouble its efforts to develop policies to reduce industrial pollution and private car usage.

@article{vera2023air,

title={Air pollution and mobility in the Mexico City Metropolitan Area in times of COVID-19},

author={Vera-Vald{\'e}s, J Eduardo and Rodr{\'\i}guez-Caballero, Carlos Vladimir},

journal={Atm{\'o}sfera},

volume={36},

number={2},

pages={343--354},

year={2023},

publisher={Centro de Ciencias de la Atm{\'o}sfera, UNAM}

}

Cataño, Duván Humberto, Rodríguez-Caballero, C.V., Peña, Daniel & Chiann, Chang.

International Journal of Wavelets, Multiresolution and Information Processing, 2021.

We introduce a high-dimensional factor model with time-varying loadings. We cover both stationary and nonstationary factors to increase the possibilities of applications. We propose an estimation procedure based on two stages. First, we estimate common factors by principal components. In the second step, considering the estimated factors as observed, the time-varying loadings are estimated by an iterative generalized least squares procedure using wavelet functions. We investigate the finite sample features by some Monte Carlo simulations. Finally, we apply the model to study the Nord Pool power market’s electricity prices and loads.

@article{catano2022wavelet,

title={Wavelet estimation for factor models with time-varying loadings},

author={Cata{\~n}o, Duv{\'a}n Humberto and Rodr{\'\i}guez-Caballero, C Vladimir and Pe{\~n}a, Daniel and Chiann, Chang},

journal={International Journal of Wavelets, Multiresolution and Information Processing},

volume={20},

number={01},

pages={2150033},

year={2022},

publisher={World Scientific}

}

Rodríguez-Caballero, C.V..

Econometrics and Statistics, 2021.

A fractionally integrated panel data model with a multi-level cross-sectional dependence is proposed. Such dependence is driven by a factor structure that captures comovements between blocks of variables through top-level factors, and within these blocks by non-pervasive factors. The model can include stationary and non-stationary variables, which makes it flexible enough to analyze relevant dynamics that are frequently found in macroeconomic and financial panels. The estimation methodology is based on fractionally differenced block-by-block cross-sectional averages. Monte Carlo simulations suggest that the procedure performs well in typical samples sizes. This methodology is applied to study the long-run relationship between energy consumption and economic growth. The main results suggest that estimates in some empirical studies may have some positive biases caused by neglecting the presence non-pervasive cross-sectional dependence and long-range dependence processes.

@article{rodriguez2022energy,

title={Energy consumption and GDP: a panel data analysis with multi-level cross-sectional dependence},

author={Rodr{\'\i}guez-Caballero, Carlos Vladimir},

journal={Econometrics and Statistics},

volume={23},

pages={128--146},

year={2022},

publisher={Elsevier}

}

Rodríguez-Caballero, C.V. & Vera-Valdés, J. Eduardo.

Econometrics, 2020.

This paper studies long economic series to assess the long-lasting effects of pandemics. We analyze if periods that cover pandemics have a change in trend and persistence in growth, and in level and persistence in unemployment. We find that there is an upward trend in the persistence level of growth across centuries. In particular, shocks originated by pandemics in recent times seem to have a permanent effect on growth. Moreover, our results show that the unemployment rate increases and becomes more persistent after a pandemic. In this regard, our findings support the design and implementation of timely counter-cyclical policies to soften the shock of the pandemic. .

@article{rodriguez2020long,

title={Long-lasting economic effects of pandemics: Evidence on growth and unemployment},

author={Rodr{\'\i}guez-Caballero, C Vladimir and Vera-Vald{\'e}s, J Eduardo},

journal={Econometrics},

volume={8},

number={3},

pages={37},

year={2020},

publisher={MDPI}

}

Rodríguez-Caballero, C.V. & Caporin, M.

Journal of International Financial Markets, Institutions and Money, 2019.

We introduce a novel multilevel factor model that allows for the presence of global and pervasive factors, local factors and semi-pervasive factors, and that captures common features across subsets of the variables of interest. We develop a model estimation procedure and provide a simulation experiment addressing the consistency of our proposal. We complete the analyses by showing how our multilevel model might explain on the commonality across CDS premiums at the global level. In this respect, we cluster countries by either the Debt/GDP ratio or by sovereign ratings. We show that multilevel models are easier to interpret compared with factor models based on principal component analysis. Finally, we experiment how the multilevel model might allow the recovery of the risk contribution due to the latent factors within a basket of country CDS.

@article{rodriguez2019multilevel,

title={A multilevel factor approach for the analysis of CDS commonality and risk contribution},

author={Rodr{\'\i}guez-Caballero, Carlos Vladimir and Caporin, Massimiliano},

journal={Journal of International Financial Markets, Institutions and Money},

volume={63},

pages={101144},

year={2019},

publisher={Elsevier}

}

Rodríguez-Caballero, C.V. & Ventosa-Santaularia, D.

Energy Economics, 2017.

We study the relationship and the causal link between Electric Power Consumption, EPC, and Gross Domestic Product, GDP (both per capita) for 17 countries in Latin America, Canada and the USA. Considering that many of these economies underwent important economic crises in the last three decades, we therefore model the EPC-GDP relationship through a VEC specification that allows for structural breaks, along with a robust testing methodology of causal links based on the concepts of weak and super exogeneity, rather than Granger causality. Evidence favorable to the growth hypothesis (EPC→GDP) is found for eight countries, while data of three countries support the conservation hypothesis (GDP→EPC). For three countries evidence is favorable to the neutrality hypothesis, but should be considered with caution. As for the remaining five countries the evidence is not conclusive.

@article{rodriguez2017energy,

title={Energy-growth long-term relationship under structural breaks. Evidence from Canada, 17 Latin American economies and the USA},

author={Rodr{\'\i}guez-Caballero, Carlos Vladimir and Ventosa-Santaul{\`a}ria, Daniel},

journal={Energy Economics},

volume={61},

pages={121--134},

year={2017},

publisher={Elsevier}

}

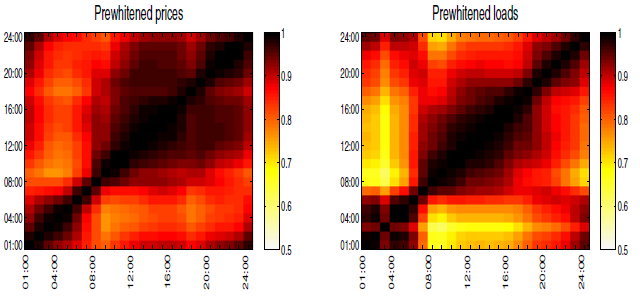

Ergemen, Yunus & Haldrup, Niels & Rodríguez-Caballero, C.V.

Energy Economics, 2016.

Equilibrium electricity spot prices and loads are often determined simultaneously in a day-ahead auction market for each hour of the subsequent day. Hence daily observations of hourly prices take the form of a periodic panel rather than a time series of hourly observations. We consider novel panel data approaches to analyse the time series and the cross-sectional dependence of hourly Nord Pool electricity spot prices and loads for the period 2000–2013. Hourly electricity prices and load data are characterized by strong serial long-range dependence in the time series dimension in addition to strong seasonal periodicity, and along the cross-sectional dimension, i.e. the hours of the day, there is a strong dependence which necessarily has to be accounted for in order to avoid spurious inference when focusing on the time series dependence alone. The long-range dependence is modelled in terms of a fractionally integrated panel data model and it is shown that both prices and loads consist of common factors with long memory and with loadings that vary considerably during the day. Due to the competitiveness of the Nordic power market the aggregate supply curve approximates well the marginal costs of the underlying production technology and because the demand is more volatile than the supply, equilibrium prices and loads are argued to identify the periodic power supply curve. The estimated supply elasticities are estimated from fractionally co-integrated relations and range between 0.5 and 1.17 with the largest elasticities being estimated during morning and evening peak hours.

@article{ergemen2016common,

title={Common long-range dependence in a panel of hourly Nord Pool electricity prices and loads},

author={Ergemen, Yunus Emre and Haldrup, Niels and Rodr{\'\i}guez-Caballero, Carlos Vladimir},

journal={Energy Economics},

volume={60},

pages={79--96},

year={2016},

publisher={Elsevier}

}

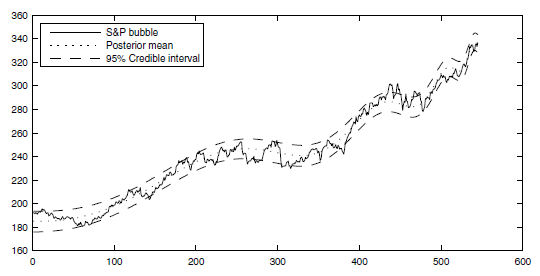

Rodríguez-Caballero, C.V.

European Physical Journal B, 2014.

This paper introduces a Bayesian approach in econophysics literature about financial bubbles in order to estimate the most probable time for a financial crash to occur. To this end, we propose using noninformative prior distributions to obtain posterior distributions. Since these distributions cannot be performed analytically, we develop a Markov Chain Monte Carlo algorithm to draw from posterior distributions. We consider three Bayesian models that involve normal and Student’s t-distributions in the disturbances and an AR(1)-GARCH(1,1) structure only within the first case. In the empirical part of the study, we analyze a well-known example of financial bubble – the S&P 500 1987 crash – to show the usefulness of the three methods under consideration and crashes of Merval-94, Bovespa-97, IPCMX-94, Hang Seng-97 using the simplest method. The novelty of this research is that the Bayesian models provide 95% credible intervals for the estimated crash time.

@article{rodriguez2014bayesian,

title={Bayesian log-periodic model for financial crashes},

author={Rodr{\'\i}guez-Caballero, Carlos Vladimir and Knapik, Oskar},

journal={The European Physical Journal B},

volume={87},

number={10},

pages={228},

year={2014},

publisher={Springer}

}

Rodríguez-Caballero, C.V. & Ventosa-Santaularia, D.

Journal of Statistical and Econometric Methods, 2014.

The asymptotic behavior of the Granger-causality test under stochastic nonstationarity is studied. Our results confirm that the inference drawn from the test is not reliable when the series are integrated to the first order. In the presence of deterministic components, the test statistic diverges, eventually rejecting the null hypothesis, even when the series are independent of each other. Moreover, controlling for these deterministic elements (in the auxiliary regressions of the test) does not preclude the possibility of drawing erroneous inferences. Granger causality tests should not be used under stochastic nonstationarity, a property typically found in many macroeconomic variables.

@article{rodriguez2014granger,

title={Granger causality and unit roots},

author={Rodr{\'\i}guez-Caballero, Carlos Vladimir and Ventosa-Santaul{\`a}ria, Daniel},

journal={Journal of Statistical and Econometric Methods},

volume={3},

number={1},

pages={97--114},

year={2014},

publisher={Scienpress Ltd}

}

Rodríguez-Caballero, C.V. & Ventosa-Santaularia, D.

Econometrics, 2013.

Polynomial specifications are widely used, not only in applied economics, but also in epidemiology, physics, political analysis and psychology, just to mention a few examples. In many cases, the data employed to estimate such specifications are time series that may exhibit stochastic nonstationary behavior. We extend Phillips’ results (Phillips, P. Understanding spurious regressions in econometrics. J. Econom. 1986, 33, 311–340.) by proving that an inference drawn from polynomial specifications, under stochastic nonstationarity, is misleading unless the variables cointegrate. We use a generalized polynomial specification as a vehicle to study its asymptotic and finite-sample properties. Our results, therefore, lead to a call to be cautious whenever practitioners estimate polynomial regressions.

@article{ventosa2013polynomial,

title={Polynomial regressions and nonsense inference},

author={Ventosa-Santaularia, Daniel and Rodr{\'\i}guez-Caballero, Carlos Vladimir},

journal={Econometrics},

volume={1},

number={3},

pages={236--248},

year={2013},

publisher={MDPI}

}

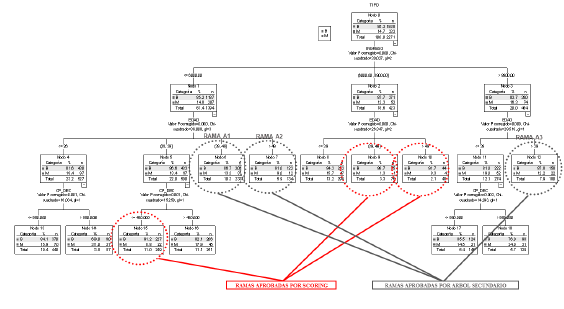

Rodríguez-Caballero, C.V. & Espin-García, O.

Cuadernos de economía, 2013.

Las decisiones de otorgamiento de crédito son cruciales en la administración de riesgos. Las instituciones financieras han desarrollado y usado modelos de credit scoring para estandarizar y automatizar las decisiones de crédito, sin embargo, no es común encontrar metodologías para aplicarlos a clientes sin referencias crediticias, es decir clientes que carecen de información en los burós nacionales de crédito. En este trabajo se presenta una metodología general para construir un modelo sencillo de credit scoring enfocado justamente a esa población, la cual ha venido tomando una mayor importancia en el sector crediticio latinoamericano. Se usa la información sociodemográfica proveniente de las solicitudes de crédito de una pequeña institución bancaria mexicana para ejemplificar la metodología.

@article{espin2013metodologia,

title={Metodolog{\'\i}a para un scoring de clientes sin referencias crediticias},

author={Espin-Garc{\'\i}a, Osvaldo and Rodr{\'\i}guez-Caballero, Carlos Vladimir},

journal={Cuadernos de econom{\'\i}a},

volume={32},

number={59},

pages={137--162},

year={2013},

publisher={Cuadernos de Econom{\'\i}a, Facultad de Ciencias Econ{\'o}micas, Universidad Nacional~…}

}

More Sections

[1] Rodríguez Caballero C.V. & Ventosa Santaulária, D. (2025).

El impacto indeleble de la regresión.

Miscelánea Matemática 81, 67–89.

DOI:

https://doi.org/10.47234/MM.8104

[1] Remittances Payments through Central Banks: An Application to the Central American Countries Exchange Rates.

Inter-American Development Bank Technical Notes, IDB-TN-1864.

With Daniel Ventosa & Arnoldo López.

Published in Economics Bulletin.

LINK:

IDB Technical Note Series

[2] Assessing the Effect of Gender Equality before the Law on Female Labor Participation and GDP per capita in Central America, Panama, and the Dominican Republic.

Inter-American Development Bank Technical Notes, IDB-TN-2128.

With Arnoldo López.

Published in Regional Statistics.

LINK:

IDB Technical Note Series

[1] Efectos del Modelo de Atención de la Fundación Camino a Casa.

En Modelo de atención para recuperar y empoderar vidas: quince años uniendo esfuerzos.

Inter-American Development Bank (2023).

With Arnoldo López Marmolejo & Emmanuel Mendez Rolón.

LINK:

IDB Book

[2] Approximation of Hate Detection Processes in Spanish and Other Non-Anglo-Saxon Languages.

En News Media and Hate Speech Promotion in Mediterranean Countries.

IGI Global (2023), 65–80.

LINK:

Book Chapter

[3] Granger causalidad espuria en la relación de cartera total y vencida de créditos.

En Administración de riesgos, Vol. IV, 2013.

[4] La inferencia bayesiana en la administración de riesgos.

En Administración de riesgos, Vol. II, 2010.

Matemáticas Financieras II

Editorial GAFRA, 2012.

Authors: C. Vladimir Rodríguez Caballero &

Osvaldo Espin García.

ISBN: 978-607-8224-42-5.

This high school textbook was created to share financial mathematics tools with young students throughout Mexico. It is used nationally as part of the sixth-semester curriculum of the Mexican Education Secretary system.

Índice: Índice (PDF)

PhD Dissertation:

On Factor Analysis with Long-Range Dependence

PhD in Economics & Business Economics (Econometrics).

Aarhus University & CREATES.

Supervisor:

Niels Haldrup

Download: PhD Dissertation (PDF)

MSc Thesis:

Ensayos sobre la Granger Causalidad

MSc in Econometrics — Universidad de Guanajuato.

Supervisor:

Daniel Ventosa Santaulària

Download: MSc Thesis (PDF)

BSc Thesis:

Inferencia Bayesiana para la volatilidad en el modelo Black & Scholes

BSc in Actuarial Science — Facultad de Ciencias, UNAM.

Supervisors:

Alejandro Villagrán Hernández &

Ramsés Humberto Mena Chávez

Download: BSc Thesis (PDF)